Renting vs Buying in 2026: The Great Housing Debate Gets a Reality Check

For generations, buying a home represented financial success, stability, and long-term security. Families considered homeownership a major life milestone. In contrast, many viewed renting as a temporary arrangement until they could afford a property of their own.

However, the housing market in 2026 looks very different.

Property prices have climbed sharply across major cities. Home loan interest rates remain relatively high. At the same time, work-from-home and hybrid work models have changed how people think about where and how they live. Consequently, more people now question whether buying a home automatically makes financial sense.

Today, the rent-versus-buy debate revolves around numbers, flexibility, and long-term goals rather than tradition alone.

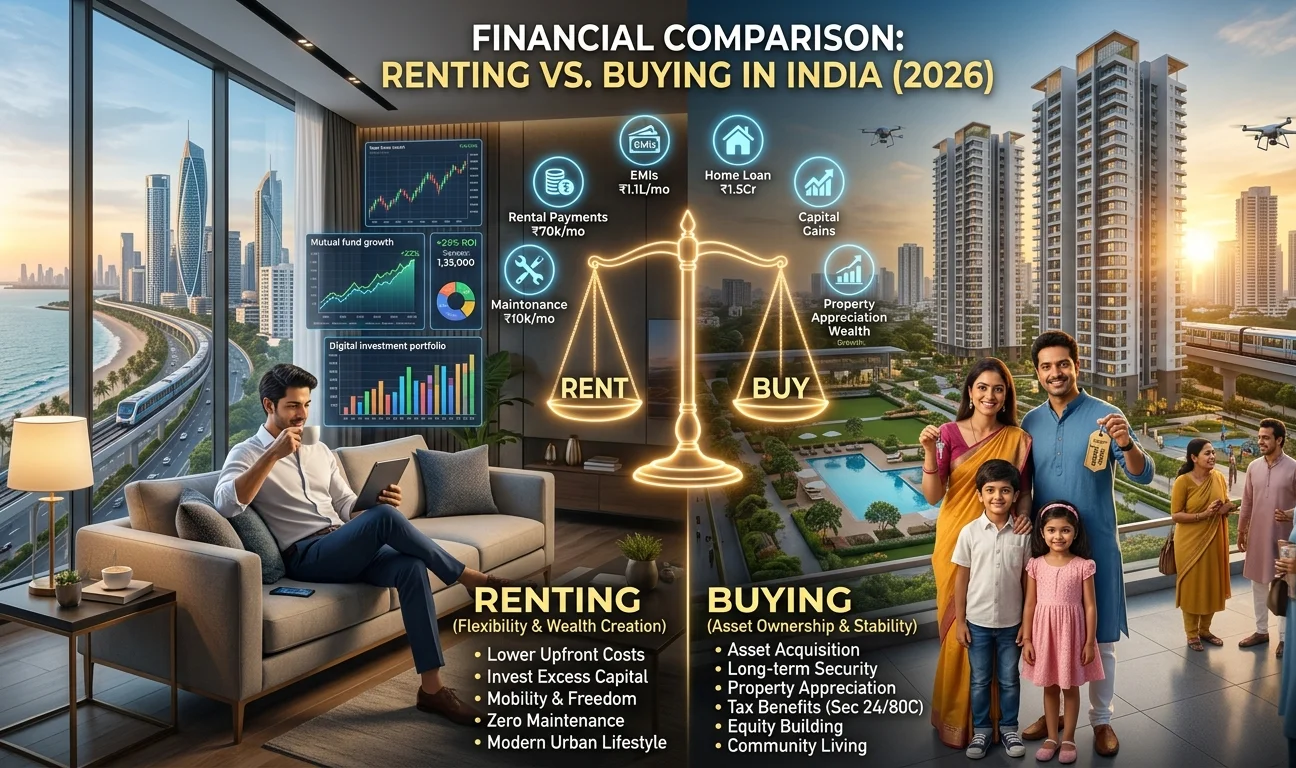

Why Buying a Home Still Remains Attractive

Buying a home offers benefits that extend beyond financial calculations.

First, homeownership provides stability. Homeowners do not need to worry about landlords increasing rent or refusing lease renewals. Instead, they enjoy complete control over their living space.

Moreover, owning a property allows families to customize interiors, renovate rooms, and create a home that reflects their lifestyle. This sense of permanence often brings emotional satisfaction that renting cannot easily match.

In India, homeownership also carries strong cultural significance. Many families view a house as a symbol of achievement and financial security. Furthermore, property often serves as a valuable asset that can be passed on to future generations.

Over time, homeowners also build equity through loan repayments. As property values rise, they may benefit from capital appreciation as well. Therefore, buying continues to appeal to individuals seeking long-term roots and wealth creation.

Why Renting Is No Longer Considered a Waste of Money

For decades, people repeated one common belief: rent is wasted money.

However, modern financial planning tells a different story.

When someone purchases a home, the monthly EMI represents only one part of the overall cost. Buyers must also account for loan interest, property taxes, maintenance charges, registration fees, stamp duty, insurance costs, and repair expenses.

Meanwhile, renters avoid most of these additional costs.

More importantly, renters can invest the money that would otherwise go toward a large down payment. They can also invest the difference between rent and ownership costs into mutual funds, stocks, or other financial instruments.

For example, consider a property worth ₹1 crore that rents for ₹30,000 per month. In many cities, the monthly ownership cost of the same property may significantly exceed the rental amount.

As a result, disciplined renters who invest consistently can potentially create substantial wealth over the long term.

Therefore, renting should not automatically be viewed as a poor financial choice.

Understanding the Price-to-Rent Ratio

One of the most effective tools for comparing renting and buying is the price-to-rent ratio.

The calculation is simple:

Price-to-Rent Ratio = Property Value ÷ Annual Rent

This ratio helps determine whether property prices justify ownership costs.

For instance, imagine a home worth ₹1 crore that rents for ₹25,000 per month. The annual rent equals ₹3 lakh. The resulting ratio exceeds 33.

A high ratio generally suggests that renting may offer better value.

On the other hand, if the same property rents for ₹55,000 per month, the ratio drops closer to 15. In this situation, buying becomes more attractive.

Although this formula cannot predict future property appreciation, it provides a useful starting point for evaluating housing decisions.

When Buying Makes Better Financial Sense

Buying tends to work best for people with long-term stability.

If you plan to remain in the same city for ten years or more, ownership often becomes financially rewarding. Property transactions involve significant expenses, including stamp duty, registration fees, and brokerage charges. A longer ownership period allows buyers to spread these costs over many years.

Additionally, properties located in rapidly developing regions often experience strong appreciation.

New metro corridors, expressways, airports, business districts, and infrastructure projects can significantly boost demand. Consequently, homeowners in these growth corridors may enjoy substantial value appreciation over time.

Buying also protects families from future rental inflation. Instead of facing annual rent increases, homeowners benefit from greater cost predictability.

Therefore, individuals with stable employment, sufficient savings, and long-term settlement plans frequently find homeownership advantageous.

When Renting Becomes the Smarter Financial Move

At the same time, renting offers several advantages that align with modern lifestyles.

Today’s professionals change jobs more frequently than previous generations. Many companies also encourage relocation across cities and regions.

As a result, flexibility has become increasingly valuable.

Renting allows individuals to move quickly without worrying about selling property or finding tenants. Moreover, renters can choose neighborhoods that match their current lifestyle and career needs.

Another advantage involves affordability.

In many metropolitan markets, property prices have increased much faster than rental rates. Consequently, renters can often live in premium locations at a significantly lower monthly cost than homeowners.

Furthermore, the rise of hybrid work arrangements has reduced the need to live close to traditional business districts. People now prioritize convenience, lifestyle, and mobility more than ever before.

Therefore, renting often proves ideal for young professionals, entrepreneurs, and anyone who values flexibility.

The Rise of Data-Driven Housing Decisions

Perhaps the biggest change in 2026 involves mindset.

Today’s buyers no longer view real estate as the only path to wealth creation.

Instead, they compare property investments with mutual funds, stocks, bonds, and other financial assets. They analyze expected returns, liquidity, risk levels, and investment horizons before making decisions.

This shift reflects a broader trend toward financial literacy.

People increasingly evaluate homes as investments rather than relying solely on emotional considerations. Consequently, housing decisions have become more strategic and financially informed.

Expert Opinion

Sanjeev Singh, Managing Director, SKJ Landbase, says:

“The decision to rent or buy should align with an individual’s financial capacity, career stability, and long-term goals. While homeownership remains a powerful wealth-building tool, buyers must carefully evaluate market conditions, infrastructure growth, and affordability. A property purchase should strengthen financial security, not create unnecessary financial pressure.”

Final Verdict

Renting and buying both offer unique advantages in 2026.

Renting often delivers greater flexibility, lower upfront costs, and stronger investment opportunities when property prices significantly exceed rental values.

Meanwhile, buying works best for individuals seeking stability, long-term wealth creation, and ownership in high-growth locations.

Ultimately, the smartest choice depends on your personal circumstances, financial goals, and future plans.

The real lesson is simple: do not buy because tradition tells you to, and do not rent because it seems easier. Instead, evaluate the numbers, understand your priorities, and choose the option that supports your long-term financial success.